What Scope 3 Accountability Actually Requires — and Why Getting It Right Is Harder Than It Looks

For most companies, direct operations account for as little as five per cent of their total climate impact. The rest sits in the value chain. Understanding why Scope 3 emissions are so difficult to measure, what the regulatory and voluntary frameworks now demand, and how to build the capability without wasting the investment.

Ask a sustainability director for their company's Scope 1 and 2 emissions, and they will almost certainly give you a number. Ask for Scope 3, and the conversation changes: estimates, methodology caveats, data gaps, supplier surveys still outstanding. This is reflects the genuinely formidable challenge that Scope 3 emissions accounting represents.

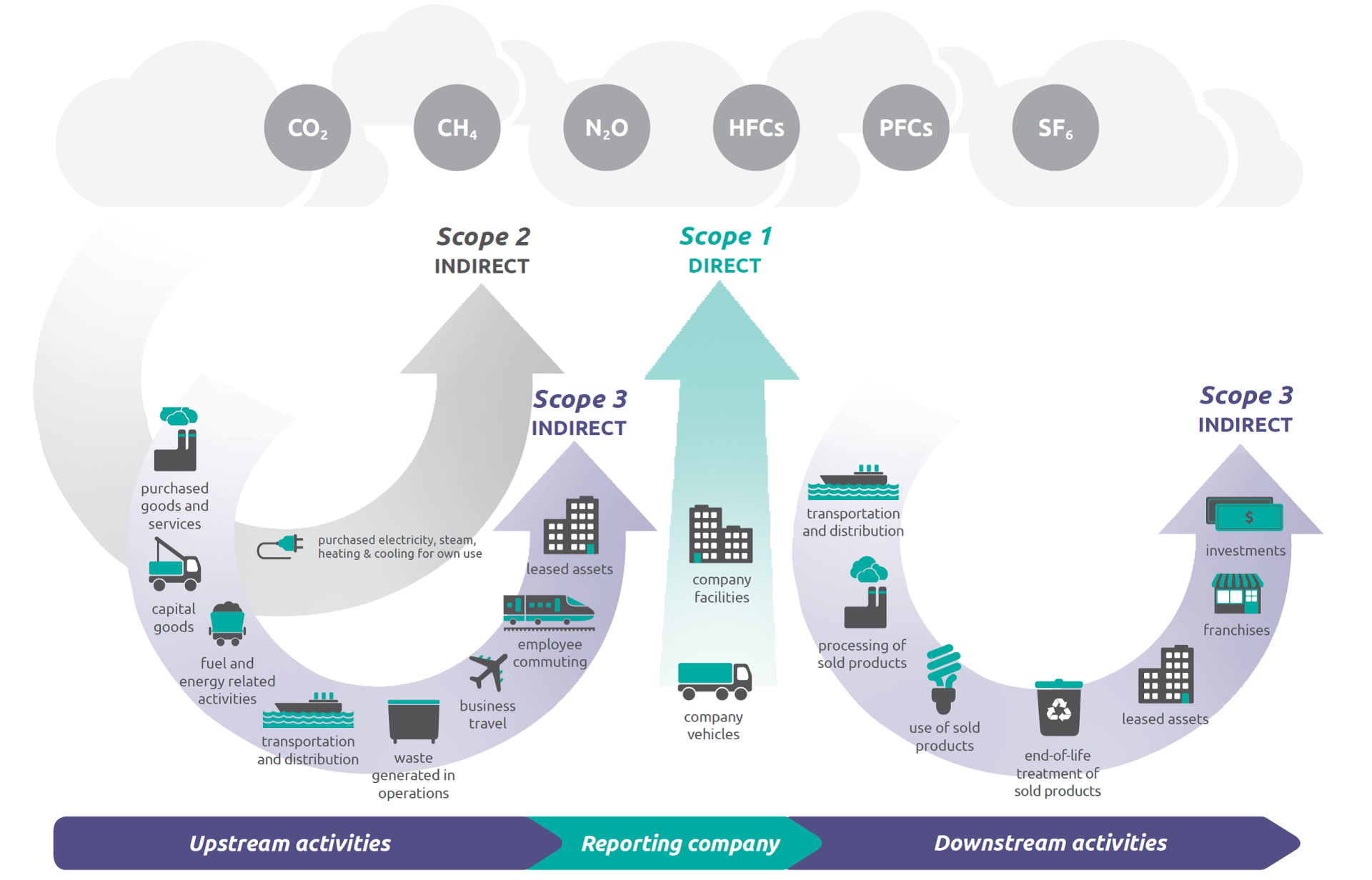

Scope 1 covers direct greenhouse gas emissions from sources owned or controlled by a company — combustion in on-site boilers, vehicle fleets, process emissions from manufacturing. Scope 2 covers the indirect emissions associated with purchased electricity, heat, and steam. These two categories are, in relative terms, tractable: they involve assets and energy consumption within a company's operational boundaries, require energy and fuel data that most finance and operations teams already collect, and the methodologies for converting that data into emissions figures are well established.

Scope 3 is categorically different. It encompasses every other indirect emission that occurs as a consequence of a company's activities — upstream in the supply chain that produces the goods and services a company buys, and downstream in how customers use its products and how those products are eventually disposed of. For most companies, Scope 3 represents between 70 and 90 per cent of their total emissions profile. In capital-light sectors where purchased goods dominate — food and beverages, apparel, financial services — the proportion frequently exceeds 95 per cent.

A company that achieves net zero across its direct operations and procures 100 per cent renewable electricity may have addressed as little as five to ten per cent of its actual climate impact. The rest sits in supplier decisions, in customer behaviour, and in what happens to its product end of life. Addressing these requires data sharing relationships and supply chain influence.

What constitutes Scope 3: Fifteen Categories

The GHG Protocol's Corporate Value Chain (Scope 3) Accounting and Reporting Standard classifies Scope 3 emissions into fifteen distinct categories, divided between upstream (relating to inputs into a company's operations) and downstream (relating to what happens after products leave the company). Each category involves a different emissions source, different data requirements, and different relationships with external parties.

Some of these categories are tractable with internal data, others require external engagement, and a few require methodological choices with significant implications for accuracy and comparability.

Category 1 — purchased goods and services — is typically the largest and most complex category for manufacturers, retailers, and consumer goods companies. It captures the emissions embedded in every input a company purchases: raw materials, packaging, components, and services. Accurately measuring Category 1 requires engaging with every material supplier, at every tier, about their own emissions performance. In global manufacturing supply chains, that can mean hundreds of direct suppliers and tens of thousands of second-tier suppliers.

Category 11 — use of sold products — is often the dominant category for energy-intensive product companies. An automotive manufacturer or appliance company must model the emissions generated when customers actually operate its products over their usable lifetime, incorporating assumptions about energy mix, usage patterns, and product longevity. These estimates are inherently probabilistic, and a company's emissions in this category depend significantly on design choices made years before products reach market.

Category 15 — financed emissions — is significant for banks, asset managers, and insurers, where the loans and investments a financial institution underwrites generate far more greenhouse gas emissions than its own operations could ever account for. The Partnership for Carbon Accounting Financials (PCAF) standard provides sector-specific methodologies for measuring financed emissions, and this category has become a central battleground for financial sector climate accountability.

Why Measurement Is Hard: The Three-Tier Data Problem

Scope 3 emissions occur outside a company's operational and legal boundaries, in organisations — suppliers, logistics providers, customers — that have their own information systems, disclosure standards, and commercial incentives.

The GHG Protocol accommodates this reality by permitting a hierarchy of data quality approaches, each offering a different trade-off between precision and practicality.

| Approach | Data source | Precision | Scalability | Strategic value |

|---|---|---|---|---|

| Spend-based estimation | Supplier spend × sector emission intensity (Exiobase, USEEIO) | Low | High | Useful for baseline and materiality screening; cannot reflect supplier-specific performance |

| Hybrid estimation | Physical activity data (tonnes, kWh, km) × process emission factors | Medium | Medium | Better accuracy for high-spend categories; still relies on average factors rather than supplier data |

| Supplier-specific primary data | Verified emissions data from individual suppliers, ideally third-party assured | High | Low | Required for credible SBTi target-setting and regulatory compliance; enables meaningful supplier engagement |

Spend-based estimation — applying average emission intensity factors from sector databases to financial spend data — is the entry-level methodology. It is practical because it uses procurement data that most companies already hold, requires no supplier engagement, and can produce a full Scope 3 inventory rapidly. The problem is that it treats every supplier in a given sector as if it has the sector-average carbon intensity, regardless of whether that supplier uses renewable energy, has invested in process efficiency, or operates a coal-powered facility. In a sector with significant emissions dispersion — as is common in steel, cement, chemicals, and agricultural commodities — this averaging introduces errors that can be substantial.

More consequentially, a spend-based methodology creates no incentive for supply chain decarbonisation. If a supplier halves its emissions intensity and a buyer continues to apply a sector-average factor to its spend, the improvement is invisible to the buyer's Scope 3 inventory.

A methodology that is practical to implement is often the methodology least likely to drive the supplier behaviour change that Scope 3 accounting is meant to catalyse.

Supplier-specific primary data including actual emissions figures provided by individual suppliers, ideally verified by a third-party assurance provider resolves this problem but introduces a scalability challenge. Collecting verified primary data from hundreds or thousands of suppliers requires supplier capacity (many SMEs, particularly in emerging markets, have never measured their emissions), supplier willingness (sharing emissions data can expose competitive information about production processes), and buyer infrastructure for collecting, validating, and integrating the data. The administrative burden of primary data collection across a complex global supply chain can be substantial.

The practical path for most companies is a staged hybrid approach: spend-based estimates for the full supply chain to establish an initial baseline and identify which categories and suppliers are most material; hybrid activity-based estimates for the highest-spend and highest-impact categories; and supplier-specific primary data selectively for strategic suppliers where the investment in data quality is proportionate to the emissions significance and the supplier relationship permits it.

The Regulatory Landscape: From Voluntary Commitment to Legal Obligation

Scope 3 reporting has moved, in a relatively short period, from a voluntary best-practice standard to a condition of regulatory compliance in an expanding set of jurisdictions. The pace and ambition of this regulatory development varies, and companies need to map their own exposure with precision. The overall direction of travel is clear and largely irreversible.

Requires large and listed companies in the EU to disclose under the European Sustainability Reporting Standards (ESRS), including ESRS E1 on climate change. ESRS E1 mandates disclosure of Scope 1, 2, and 3 emissions, transition plans, and climate-related targets. The value chain provisions extend obligations indirectly to non-EU suppliers of in-scope companies.

Applies a carbon price to imports of carbon-intensive goods into the EU — initially covering cement, iron and steel, aluminium, fertilisers, electricity, and hydrogen. Importers must declare the embedded carbon content of covered goods, creating a direct financial incentive for non-EU producers to measure and reduce their production-related emissions.

Requires companies placing seven commodity categories — beef, soya, palm oil, coffee, cocoa, wood, and rubber — on the EU market to demonstrate that those commodities did not contribute to deforestation. Compliance requires geolocation data and supply chain traceability at a level that most commodity buyers have not previously maintained.

Requires disclosure of Scope 3 emissions for companies where Scope 3 is material to their climate-related risks — a determination that, in practice, applies to most large companies. Increasingly being adopted by national regulators as the basis for mandatory disclosure frameworks, including in Australia, Canada, Singapore, and the UK.

Requires companies committing to the Corporate Net-Zero Standard to set Scope 3 targets covering at least two-thirds of their total Scope 3 inventory. Near-term targets require a 90% reduction in Scope 3 emissions from a base year. The FLAG guidance extends requirements to agriculture and land-use emissions specifically.

The SEC's climate disclosure rule, finalised in 2024, has faced legal challenges, but the direction of US regulatory travel reflects a broader convergence toward mandatory emissions disclosure for listed companies, with Scope 3 disclosure required where material.

Whereas other frameworks require disclosure, the SBTi requires commitment to reduction targets validated against 1.5°C aligned pathways. Its Scope 3 target setting requirements effectively make supply chain decarbonisation a condition of credible net-zero commitment for most companies.

For companies in high Scope 3 sectors such as food and agriculture, apparel and textiles, extractives, and financial services; the SBTi's FLAG (Forest, Land, and Agriculture) guidance introduces an additional layer of specificity. It addresses the emissions associated with deforestation and land conversion in agricultural supply chains, which account for a disproportionate share of Scope 3 for food companies sourcing from tropical commodity regions. FLAG targets must be set alongside conventional emissions targets and require traceability data that goes well beyond what most agricultural supply chains currently provide.

The Dual Exposure of Emerging Market Companies

For companies primarily in Sub-Saharan Africa, South Asia, Southeast Asia, and Latin America, Scope 3 accountability creates a distinctive dual exposure.

The first dimension is as a supplier. Companies in these regions are, in many cases, embedded in the upstream value chains of multinationals that are now legally or commercially obligated to measure and manage their Scope 3 emissions. A Ghanaian cocoa processor, a Kenyan tea producer, a Bangladeshi garment manufacturer, or a South African steel supplier are all potential targets of supplier engagement programmes driven by their customers' Scope 3 obligations. This creates both a compliance pressure — to provide emissions data that customers need for their own inventories — and a strategic opportunity for early movers to differentiate themselves as low-carbon suppliers in procurement processes where sustainability performance is increasingly a criterion alongside price and quality.

CBAM creates a particularly direct financial mechanism. Producers of covered commodities exporting to the EU will face a carbon cost on the embedded emissions in those goods from 2026, calculated against the EU carbon price. Exporters who can demonstrate low embedded carbon — through verified primary emissions data — face a lower CBAM liability. This makes emissions measurement and reduction investment a matter of commercial cost management.

The second dimension is as a buyer and manufacturer. Emerging market companies that purchase goods and services, manage supply chains, and sell products face the same Scope 3 challenge as any large corporate — with additional complexity. Local supplier data infrastructure is often underdeveloped: SME suppliers often operate outside formal emissions reporting regime, sector emission intensity databases may not exist at the required granularity, and the professional ecosystem of sustainability consultants, assurance providers, and technology platforms is less mature.

At the same time, the regulatory exposure for emerging market companies is generally — for now — less immediate than for their multinational counterparts. The window that exists before domestic regulatory requirements catch up with international standards is an opportunity to build Scope 3 capability in a lower-pressure environment.

Building the Capability: A Maturity Journey, Not a Single Project

Corporate Scope 3 capability is built over multiple reporting cycles, through progressive improvement in data quality, supplier engagement depth, and internal ownership.

The first stage is establishing a baseline inventory. This typically relies on spend-based estimates across most categories, supplemented by available activity data, and gives a picture of where a company's Scope 3 emissions are concentrated. The value of this stage is materiality identification. A company that does not know whether its largest Scope 3 source is purchased raw materials, product use, or logistics cannot prioritise its data improvement or reduction efforts rationally.

The second stage is targeted data quality improvement in material categories. Having identified the categories and supplier relationships that account for the majority of estimated Scope 3 emissions, a company can invest in more precise measurement where it matters: primary data collection from strategic suppliers, more granular activity data for high-emission logistics routes, product lifecycle modelling for category 11 use-phase emissions. This stage typically requires technology investment — supplier data portals, lifecycle assessment tools, and systems integration between procurement and sustainability functions.

The third stage is integrating Scope 3 into commercial and procurement decision-making. Procurement criteria that include supplier carbon performance; product development processes that incorporate end-of-life emissions into design decisions; supplier development programmes that build measurement capacity in the supply chain and reward low-carbon suppliers with preferred commercial terms. This stage requires organisational change well beyond the sustainability function. It requires procurement, product development, finance, and executive leadership to work closely and treat emissions as a material input into commercial decisions.

Preparing for Scope 3 Accountability: Preliminary reflection for Corporate Leaders

Before committing resources to Scope 3 measurement and reporting, it is worth addressing a prior question of whether and how urgently the investment is warranted for your specific business. Moving too late creates regulatory and commercial exposure but investing without strategic clarity may be a diservice to the business. Teams should discuss the following:

Moving forward, management of scope three emissions will become a competitive advantage driven by increasing demand for supply chain transparence. Major buyers are already compelling their suppliers to disclose information under CPD's supplier Programme.

Stay up and close

You will now receive monthly updates directly in your inbox.