What Is Blended Finance? Definition, Principles, Market Data, and How It Works

Blended finance uses public or philanthropic capital to reduce risk for private investors, so projects that would not otherwise attract commercial money can get built. This article gives the definition, the OECD DAC principles, the instruments and actors involved, market size and trends, development impact, and the effect of declining aid budgets and shifting geopolitics on the model.

volume*

deal flow*

MDB/DFI $*

1. Definition

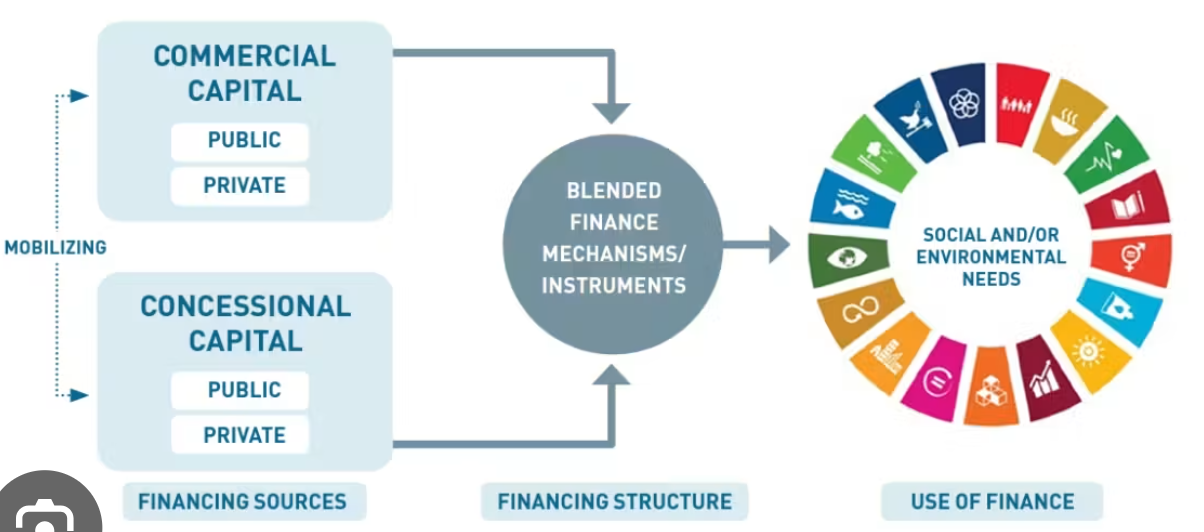

Blending finance is the is the catalytic use of public or philanthropic capital to mobilze additional private sector investment. The OECD Development Assistance Committee (DAC) defines it as the strategic use of development finance to mobilise additional finance towards sustainable development in developing countries. The OECD's definition covers development capital mobilising other public or development-oriented capital, such as one multilateral development bank's (MDB) funds drawing in another MDB's co-financing.

Three characteristics a transaction must meet to count as blended finance:

- Contribution to the Sustainable Development Goals (SDGs). The transaction advances at least one SDG target, although not every investor in the structure needs to share that objective — a private investor in a blended structure may be seeking a market-rate financial return only.

- An expected positive financial return. Different investors in the same structure carry different return expectations, ranging from concessional to market-rate.

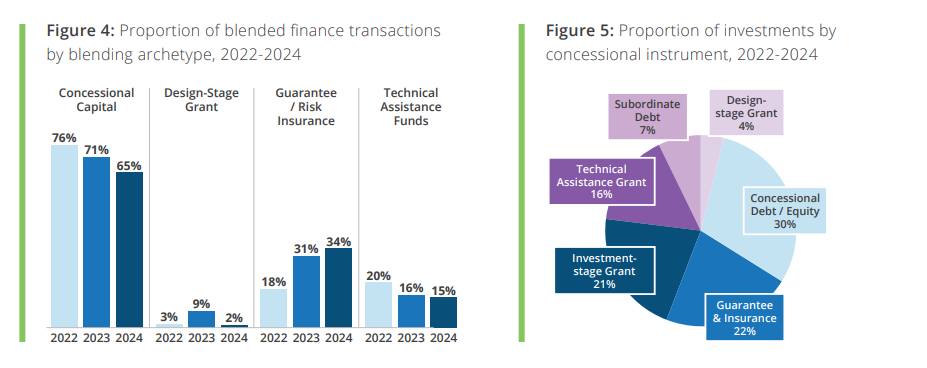

- A catalytic capital element. This takes one of four forms: concessional capital provided on below-market terms to lower the cost of capital; guarantees or risk insurance on below-market terms; technical assistance funds attached to the transaction; or grant-funded design-stage or project-preparation grants.

Blended finance is not a synonym for development finance generally, and it is not a separate pool of money. It is a structuring method applied to a transaction or fund — combining capital with different risk-return expectations within a single vehicle so that an investment that would not clear a commercial hurdle rate on its own can attract investors who require market-rate or near-market-rate returns. Goal 17 (Partnerships for the Goals), Goal 8 (Decent Work and Economic Growth), Goal 9 (Industry, Innovation, and Infrastructure), and Goal 5 (Gender Equality) have been the most targeted SDGs in recorded blended finance transactions; the model is less suited to SDGs without a revenue-generating or investable component, such as Goal 16 (Peace, Justice and Strong Institutions).

2. Principles and Frameworks

The OECD DAC Blended Finance Principles, approved in 2017 and supported by detailed Guidance first published in 2020 and updated in September 2025, set out five principles that providers of development finance are expected to apply when structuring blended transactions:[2]

- Anchor blended finance use to a development rationale. Development objectives and expected results must be defined as the basis for deploying development finance, agreed jointly with stakeholders.[3]

- Design blended finance to increase the mobilisation of commercial finance. Structures should be designed to draw in private capital rather than substitute for it.[4]

- Tailor blended finance to the local context. Structures need to reflect the regulatory, market, and institutional conditions of the country in question.[5]

- Focus on effective partnering for blended finance. Transactions involve multiple counterparties with different mandates, requiring coordination mechanisms.

- Monitor blended finance for transparency and results. Providers are expected to report on both financial mobilisation and development outcomes.

The 2025 update to the Guidance states showed that blended finance has not scaled as rapidly as hoped and has mobilised relatively limited private finance, and describes the field as having remained a cottage industry with largely fragmented interventions, alongside a lack of standardisation and transparency.[6] This is the OECD's own characterisation, not an external critique, and it frames the rest of the 2025 Guidance around addressing those specific gaps.

The DFI Working Group on Blended Concessional Finance for Private Sector Projects — a coalition of multilateral and bilateral development finance institutions — publishes joint principles specifically for private-sector blended transactions, focused on minimum concessionality (using the smallest amount of concessional funding necessary) and commercial sustainability. The International Finance Corporation (IFC), part of the World Bank Group, applies these principles to its own blended concessional finance facilities.[7]

3. Instruments and Structures

| Instrument | Function | 2024 Market Share[8] |

|---|---|---|

| Concessional debt or equity | Capital provided below market rate, often as first-loss debt or equity, to absorb initial losses ahead of commercial investors | Most common archetype historically[1] |

| Guarantees / risk insurance | Credit enhancement on below-market terms that reduces downside risk for private lenders or investors without disbursing capital upfront | 46% of concessional instruments used in blended vehicles[8] |

| Technical assistance funds | Grant-funded support, deployed pre- or post-investment, to strengthen commercial viability and development outcomes | Attached to a subset of transactions[1] |

| Design-stage / project-preparation grants | Grant funding for transaction design or preparation before financial close | Used across early-stage deal pipeline[1] |

| Structured funds / collective investment vehicles (CIVs) | Pooled vehicles with layered tranches (junior/first-loss, mezzanine, senior) or flat pari passu structures, mixing concessional and commercial capital | Assets under management in OECD-surveyed CIVs reached USD 75 billion in 2020, up 24% from 2018[9] |

Guarantees have grown in relative importance. Convergence recorded USD 1 billion in concessional guarantees in 2024, a 42% increase from 2023.[8] Because guarantees do not require upfront capital outlay in the way concessional debt does, their growing use changes how leverage and mobilisation ratios in the market are measured. When concessional guarantees are excluded, the leverage ratio across recorded deals rises to 4.37 and the private-sector mobilisation ratio rises to 2.5.[8]

Development agencies and multi-donor funds have also shifted the type of concessional instrument they disburse. Between 2022 and 2024, the share of their concessional capital delivered as grants fell from 41% to 10%, while the share delivered as guarantees rose from 11% to 27% and as senior debt from 19% to 24%.[10] There is a shift toward risk-sharing instruments and away from grants.

4. The Ecosystem of Actors

Blended finance transactions bring together five categories of participant, each with a distinct role and capital expectation.

- Development finance institutions and multilateral development banks. Institutions such as the World Bank Group, the European Bank for Reconstruction and Development, and regional development banks provide both concessional and commercial-development-oriented capital, and frequently anchor transactions.

- Donor governments and bilateral agencies. National development agencies contribute concessional capital, technical assistance funding, and guarantees, often channelled through multi-donor trust funds.

- Multilateral climate and environmental funds. Vehicles such as the Green Climate Fund (GCF), the Global Environment Facility (GEF) and its associated funds, and the Adaptation Fund increasingly deploy non-grant instruments (NGIs) alongside grants.

- Philanthropic foundations. provide grant capital, first-loss tranches, and guarantees, typically in smaller volumes than DFIs and donor agencies but with higher risk tolerance.

- Private investors. This category spans commercial banks, institutional investors (pension funds, insurers, asset managers), and local private actors domiciled in emerging markets. In 2024, commercial capital from private-sector investors outpaced DFIs and MDBs in capital deployment, with USD 6.9 billion in private investment recorded for that year.[10]

Within climate-focused blended finance specifically, institutional investors committed USD 1.6 billion in 2024, up from USD 2 million in 2022, and commercial banks contributed USD 2.4 billion.[11] Local private actors domiciled in emerging markets have grown as a share of overall climate blended finance investment, from 17% in 2019–2021 to 29% in 2022–2024.[11]

Legal counsel and standard-setting bodies form a supporting layer of the ecosystem. These include institions such as the Global Alliance of Impact Lawyers (GAIL) maintains a Blended Finance Working Group that publishes regional case studies and legal-pathway analysis used by transaction counsel structuring blended deals across jurisdictions.[12]

5. Market Volume and Flow Trends

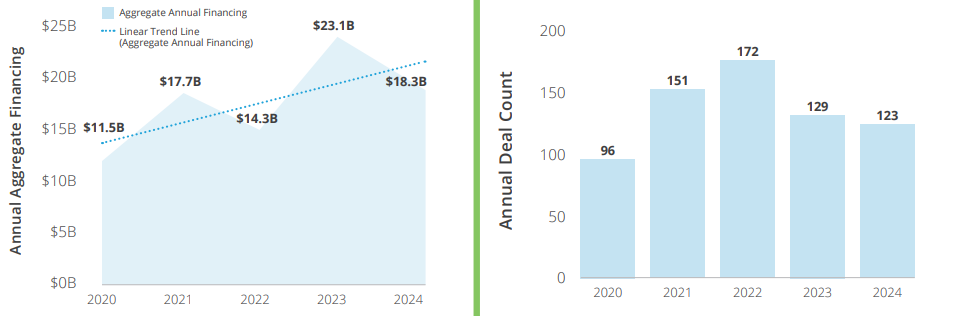

Convergence's Historical Deals Database recorded approximately 1,350 blended finance transactions totalling USD 249.2 billion in cumulative volume as of 2025.[8] Annual deal flow has fluctuated rather than risen in a straight line. The market reached a record high in 2023 at USD 23.1 billion across 129 deals, then declined to USD 18 billion across 123 deals in 2024 — a level still above the five-year average and well above the USD 11.5 billion recorded in 2020.[10][8] Median deal size rose from USD 38 million (2020–2023 average) to USD 65 million in 2024, lifted in part by three transactions each exceeding USD 1 billion.[10]

Regional and sectoral concentration. Sub-Saharan Africa has been the most targeted region across the full historical dataset, with Asia and Latin America identified as more recent growth areas.[1] Top sectors include financial services followed by energy.[1] Within climate blended finance specifically, the share of climate blended finance activity in least developed countries (LDCs) fell from 23% to 5%, while the share of deals in lower-middle-income countries rose from 62% to 73%.[11]

Europe and Central Asia which have have been historically underrepresented in blended finance — saw its share of global deals rise from 10% in 2022 to 23% in 2024, with associated financing flows rising from USD 2.8 billion to USD 5.9 billion over the same period, a shift Convergence links to the war in Ukraine.[10]

Structured funds, a specific instrument category within the market, grew from USD 612 million in aggregate captured financing in 2014 to nearly USD 2.2 billion in 2023, a rise of more than 260%, with Convergence's database recording approximately 113 such funds opened between 2014 and 2023.[9]

6. Financial and Development Impact

Across 2019–2021, blended finance structures enabled MDBs and DFIs to mobilise USD 0.50 of private capital for every USD 1 committed from their own balance sheets.[13] When concessional guarantees are excluded from the calculation, Amundi Research Center's analysis of Convergence data shows the private-sector mobilisation ratio rising to 2.5.[8]

The OECD's data on mobilised private finance for development shows that mobilisation levels remain limited relative to the scale of development and climate financing needs identified by the OECD and others.[14] The 2025 Blended Finance Guidance attributes this gap to the market's continued reliance on non-standardised transaction structures that are costly to replicate at scale.[6]

Development outcome reporting in blended finance is uneven across the market. The OECD DAC Principle on monitoring calls for providers to report on both financial mobilisation and development results, but standardised, comparable results reporting across the full universe of blended transactions does not yet exist.

The IFC's November 2025 report, "Mobilizing Private Capital: The Role of Blended Finance in a Changing Global Landscape," documents how blended instruments — debt, equity, performance-based incentives, and guarantees — allow specific high-impact projects to proceed where they would not otherwise reach financial close on commercial terms alone.[7]

7. Multilateral Cooperation and Geopolitical Shifts

Blended finance depends on a steady supply of concessional and grant capital from donor governments and multilateral institutions to perform its risk-absorbing function. Total official development assistance (ODA) from the 34 members of the OECD Development Assistance Committee fell to USD 174.3 billion in 2025, a decline of 23.1% in real terms compared with 2024. This is the largest single-year reduction on record.[15]

Bilateral ODA fell 26.4% to USD 126.4 billion; bilateral grants specifically fell 29.1%; bilateral ODA for core development programmes, projects, and technical cooperation — excluding humanitarian aid, in-donor refugee costs, and debt relief — fell 26.3%.[16][17] Multilateral ODA fell 12.6% in 2025, its second consecutive annual decline, with core contributions to the UN system down 27%, also the largest annual drop on record in that line.[15][17] Contributions to the World Bank and regional development banks increased over the same period, even as UN-channelled multilateral funding.[17]

The United States accounted for roughly three-quarters of the 2025 global decline. US ODA fell from approximately USD 60 billion to just under USD 30 billion in a single year — a 56.9% reduction — which OECD DAC analysis attributes primarily to the disolution of USAID.[18][19] As a result of this reduction, Germany became the largest DAC donor in 2025 at USD 29.1 billion, followed by the United States at USD 29 billion, the United Kingdom at USD 17.2 billion, Japan at USD 16.2 billion, and France at USD 14.5 billion.[15]

Non-DAC providers grew their reported contributions to USD 13.3 billion in 2025, a 4.5% increase over 2024, driven by an expansion in their bilateral ODA (+5.4%) that offset a decline in their multilateral ODA (-13.2%).[21]. The OECD projects a further 5.8% decline in ODA for 2026, a forecast that, as of publication, does not yet incorporate the financial effects of the Middle East conflict.[18]

Several political factors are cited in current analysis as drivers of the contraction. Global Policy Journal analysis published in June 2026 identifies rising ideological hostility to multilateralism, with the disolution of USAID alone accounting for more than three-quarters of the 2025 ODA decline; defence-spending increases that constrain other discretionary budgets, including the NATO Hague Summit's 2025 agreement on a 5% of GDP defence-spending target by 2035; and explicit trade-offs in individual donor budgets, including the United Kingdom's stated linkage between ODA reductions and defence spending increases, and France's 2026 finance bill, which cuts ODA while raising defence spending.[22]

Non-traditional sources of concessional and development finance have not yet substituted for the contraction at scale. The Arab Coordination Group provided USD 19.6 billion in 2024, and the OPEC Fund disbursed a record USD 2.3 billion.[22] Chinese overseas development finance has settled at approximately USD 6 billion annually and is reported to be reorienting toward strategic supply-chain investment rather than concessional development lending.[22] A BRICS meeting in Delhi in April 2026 did not reach consensus on a coordinated financing response, which signals the current limits of BRICS+ as a coordinated financing bloc.

This contraction in concessional and grant capital directly reduces the supply of the catalytic capital the blended financing model depends on.

8. Challenges

- Market fragmentation and limited standardisation limits coordination and replication of successful blended structures.

- Concentration of concessional capital among public providers. In many cases, concessional bilateral public capital mobilises public commercial funding from MDBs and DFIs rather than private investment. Hence, the "catalytic" function is not always reaching private capital as intended.

- Limited private-sector mobilisation strategy among donors.

- Low local capital participation. The OECD's 2020 survey of blended finance funds and facilities found that private commercial investors contributed less than 6% of total capital in collective investment vehicles, despite such vehicles being identified as essential structures for blended finance flows.[9]

- Exposure to ODA volatility. Because concessional and grant capital from donor governments underwrites the catalytic function of blended structures, a 23.1% real-terms decline in ODA in a single year, as recorded in 2025, directly constrains the supply of capital available to structure new transactions.[15]

10. Frequently Asked Questions

The use of catalytic capital from public or philanthropic sources to increase private sector investment in sustainable development.

Approximately 1,350 transactions totalling USD 249.2 billion in cumulative volume.[8] Convergence's summary cites a rounded figure of approximately USD 200–280 billion mobilised to date, depending on the dataset cut and publication date referenced.

Concessional finance is capital provided on below-market terms. It is one of the catalytic capital types used within a blended finance structure, not a synonym for blended finance itself. A blended finance transaction combines concessional capital with commercial or market-rate capital in the same structure.

ODA fell 23.1% in real terms in 2025, driven primarily by United States cuts linked to the dismantling of USAID, alongside reductions from other donors tied to rising defence spending and domestic fiscal pressure. Because blended finance structures depend on donor-supplied concessional capital and guarantees to absorb risk, a contraction in that supply directly constrains the volume of new blended transactions that can be structured.

Financial services has been the most frequently targeted sector historically, followed by energy. Sub-Saharan Africa has been the most frequently targeted region, with Asia and Latin America identified as recent growth areas. Within climate blended finance, lower-middle-income countries received 73% of 2024 deals, up from 62% in 2023, while the LDC share of activity fell from 23% to 5% over the same period.

Sources

- [1] Convergence. Blended Finance Primer. convergence.finance/blended-finance

- [2] OECD. The OECD DAC Blended Finance Guidance. oecd.org

- [3] OECD (2025). Principle 1: Anchor blended finance use to a development rationale. oecd.org

- [4] OECD (2025). Principle 2: Design blended finance to increase the mobilisation of commercial finance. oecd.org

- [5] OECD (2025). Principle 3: Tailor blended finance to the local context. oecd.org

- [6] OECD (2025). Overview: OECD DAC Blended Finance Guidance 2025. oecd.org

- [7] IFC (Nov 2025). Mobilizing Private Capital: The Role of Blended Finance in a Changing Global Landscape. ifc.org

- [8] Amundi Research Center (Oct 2025). How Can Investors Lean Into Blended Finance Structures. research-center.amundi.com

- [9] OECD (2025). Principle 2 — CIV and structured fund data (Dembele 2022; Convergence 2024). oecd.org

- [10] Convergence (21 May 2025). Press Release — Blended finance market held strong in 2024. convergence.finance

- [11] Convergence (3 Nov 2025). Press Release — State of Climate Blended Finance 2025. convergence.finance

- [12] Convergence. Homepage and Blended Finance Accelerator. convergence.finance

- [13] Amundi Research Center (Oct 2025). MDB/DFI mobilisation ratio, 2019–2021. research-center.amundi.com

- [14] OECD. Mobilisation of private finance for development Dashboard. oecd.org

- [15] Focus 2030 (9 Apr 2026). Historic drop in Official Development Assistance in 2025. focus2030.org

- [16] OECD (9 Apr 2026). International aid fell sharply in 2025, says OECD. oecd.org

- [17] OECD (9 Apr 2026). A historic decline in foreign aid: Preliminary 2025 ODA data. oecd.org

- [18] Devex (9 Apr 2026). ODA plummets by almost a quarter, driven by billions in US cuts. devex.com

- [19] Health Policy Watch (10 Apr 2026). Record ODA Cuts: Top Donors Slash Aid As Global Health Risks Grow. healthpolicy-watch.news

- [20] ECDPM (10 Apr 2026). The consequences of international aid cuts. ecdpm.org

- [21] OECD DCD(2026)8. Non-DAC providers' 2025 development finance flows. one.oecd.org

- [22] Global Policy Journal (18 Jun 2026). Three Implications of the Oil Shock for the Turbulent Political Economy of Development Cooperation. globalpolicyjournal.com

- [23] Convergence. Network Voices — local currency guarantees; Germany climate blended finance initiative. convergence.finance

- GAIL. Convergence report analysis and Blended Finance Working Group. gailnet.org

- OECD (2025). Cuts in Official Development Assistance — Full Report. oecd.org