ESG and Anti-ESG Shareholder Proposals in the 2026 Proxy Season: What the Vote Data Shows

The 2026 U.S. proxy season has run under a materially different SEC posture than prior years, after the agency stopped issuing substantive no-action guidance on most grounds for excluding shareholder proposals. Anti-ESG proposals remain as common as ever, but the numbers through the season's midpoint show a familiar pattern: high visibility, very low shareholder support.

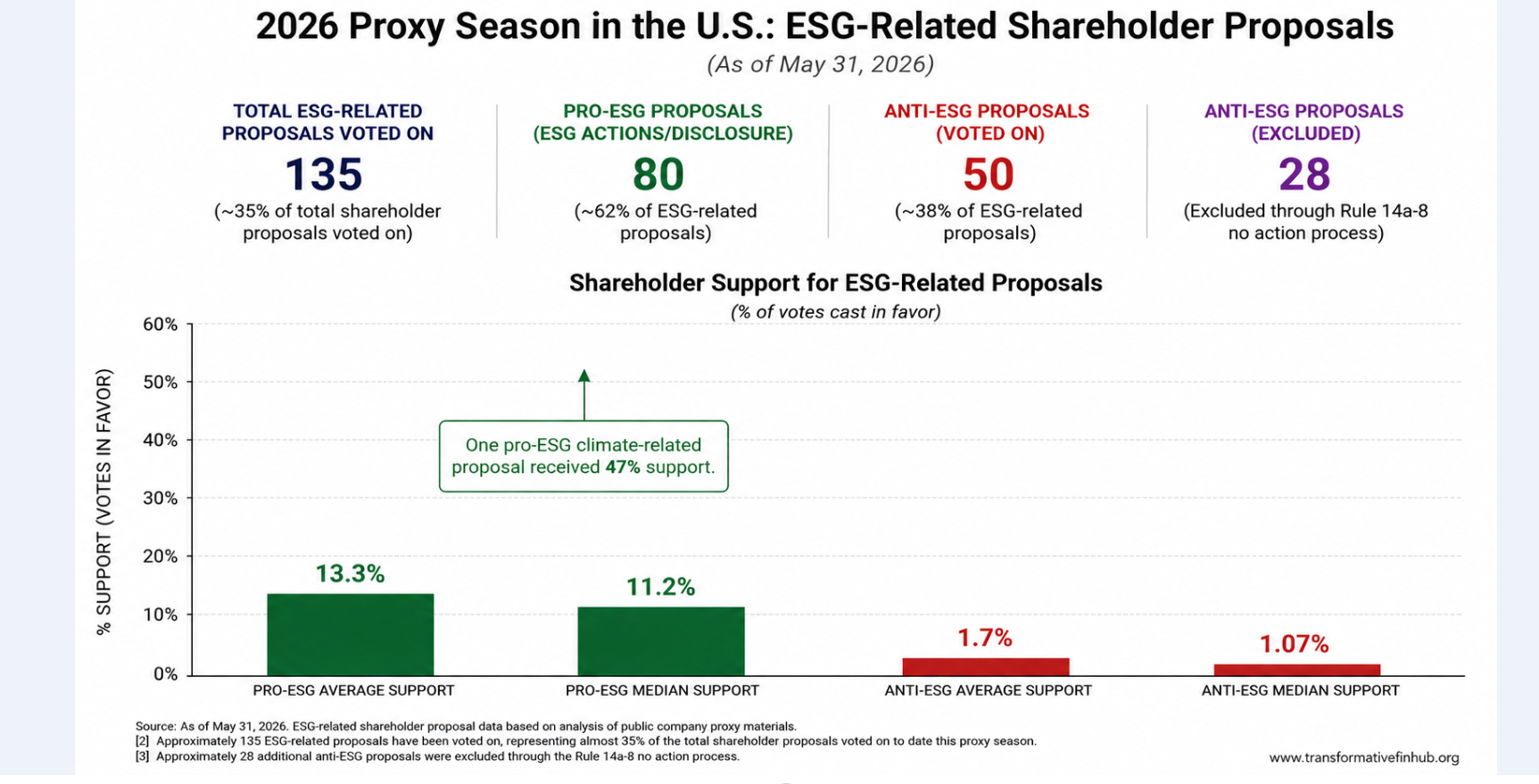

1. A Different Season, a Familiar Pattern

In November 2025, the SEC's Staff announced that, for the 2025–2026 proxy season, it would no longer provide substantive views on most grounds companies cite to exclude shareholder proposals under Rule 14a-8 of the Securities Exchange Act. Historically, companies wanting to leave a proposal out of their proxy statement asked the SEC Staff for a "no-action" letter confirming the Staff would not pursue enforcement over the exclusion. With that substantive review effectively paused for most exclusion grounds, companies still had to notify the SEC and proposal sponsors of an intended exclusion, but without the Staff's customary steer on whether the exclusion would hold up.

That procedural shift has changed how companies and proponents interact this season, but it has not changed the underlying volume of anti-ESG proposals, which remains as high as in recent years. Anti-ESG proposals generally push back on, or question the value of, corporate ESG-related policies — from emissions and net-zero commitments to diversity programs, shareholder-rights provisions, and broader corporate-responsibility practices.

Support levels tell the clearer story. As in 2024 and 2025, no ESG-related proposal — pro- or anti-ESG — passed in 2026. Anti-ESG proposals averaged about 1.7% support (median 1.07%). Proposals backing ESG-related action fared better but still fell far short of passing, averaging about 13.3% support (median 11.2%); one climate-related pro-ESG proposal reached 47%, the standout result of the season so far.

2. Exclusion Notices Without Substantive Review

Companies are still required to notify the SEC and proponents when they intend to leave a proposal out of proxy materials, even though the Staff is largely withholding its view on the merits. Around 190 Rule 14a-8 exclusion notices have been filed in 2026 to date; roughly 60 of those, about 35%, relate to ESG topics. Of that ESG-related subset, about 53% targeted anti-ESG proposals and 47% targeted pro-ESG proposals — a near-even split.

Several exclusion topics recurred across multiple companies: requests that companies assess the reputational, human-capital, operational, and legal risk of excluding religious charities from employee-gift matching; requests for disclosure of the expected return on investment from climate commitments and net-zero targets; and requests for a report on risks tied to reproductive rights and gender-related healthcare policy. The last two categories — gender-related healthcare and, separately, immigration policy — are new to the 2026 season rather than holdovers from prior years.

Because the Staff is not weighing in on the substance of most exclusion requests, companies have leaned more heavily on how the Staff treated similar proposals in past seasons. Where no earlier proposal on a given topic exists, there is no way to know how the Staff would have ruled — yet several companies proceeded with exclusion anyway, absent that precedent.

3. Where Anti-ESG Proposals Are Concentrated

Looking at both excluded and voted anti-ESG proposals together, the bulk still cluster around the topics most associated with the anti-ESG label: opposition to DEI programs and to corporate climate-risk mitigation. The chart below breaks down proposal counts by theme so far in 2026.

Consumer values, free speech, and religious exercise

This has been the season's sharpest area of growth: close to a quarter of all anti-ESG proposals now focus on the public positions taken by a company, its officers, or its directors, and how those positions might affect employees, customers, and ultimately financial performance. Three recurring concerns sit inside this category — the risk profile of corporate charitable giving, the risk of a company's stated values diverging from its customers' values (sometimes framed as viewpoint discrimination), and the risk of religious discrimination against employees.

On charitable giving specifically, close to 20 companies have received a proposal this season asking for an analysis of the benefits, costs, and legal, reputational, and competitive risk tied to their charitable-giving or employee-gift-match programs — more than three times the number of companies that saw a comparable proposal in 2025. It is a broader version of last year's most common anti-ESG proposal, which asked more narrowly about giving-related discrimination on the basis of speech or religion. Notably, around ten of this year's versions were excluded under Rule 14a-8, even though the SEC denied no-action relief to similar proposals in 2025. Where these proposals did go to a vote, support has stayed low — no higher than 2.2% in 2026.

On customer-value alignment, two companies faced a proposal asking them to evaluate whether their policies, public statements, and partnerships are out of step with their customer base, and what legal, regulatory, or reputational exposure that might create. Three more companies received a related proposal — a 2026 version of a 2025 staple — asking how the company manages the risk of "viewpoint discrimination" against users or customers under hate-speech or misinformation policies. Voted proposals in this category again drew under 3% support.

A smaller but notable cluster — two proposals — asked companies to evaluate the risk of not permitting faith-based employee resource groups, arguing that excluding such groups is itself a form of discrimination inconsistent with a stated commitment to equal treatment. Both proposals received less than 1% support.

Healthcare and reproductive rights

Proposals tied to healthcare and reproductive rights make up roughly 13% of this season's anti-ESG proposals and represent one of the most significant new categories in 2026 — there is little precedent for this theme in recent seasons, and no comparable rise has appeared on the pro-ESG side. Two variants dominate: proposals asking companies to detail risk from distributing mifepristone and to describe any risk strategy beyond litigation and legal compliance, and proposals asking about risk tied to offering gender-affirming care within employee health benefits. Only four proposals in this category reached a vote, all receiving under 1.5% support.

Anti-DEI proposals

Anti-DEI proposals have fallen sharply as a share of the anti-ESG total — from over 40% of voted anti-ESG proposals in 2025 to about 14% in 2026. Support has fallen alongside that decline, from a 2025 high of roughly 3% to a 2026 average of 1.26% and a high of about 2.2%.

The framing has also softened. Where 2025 proposals often called outright for companies to abolish DEI policies, 2026 versions are more commonly built around financial metrics — asking companies to evaluate DEI programs using net-present-value or return-on-investment analysis, factoring in litigation risk and potential backlash, or asking companies to assess the risk of tying ESG and DEI metrics to executive compensation. That shift toward value-based framing tracks broader SEC commentary this season linking corporate action to shareholder value and long-term financial performance rather than non-financial objectives — though it is not possible to say definitively whether proponents are responding to that messaging or simply reflecting a broader change in the political environment.

Climate-related risk

Roughly 30% of 2026 anti-ESG proposals oppose company responses to climate risk, up from about 20% at the same point in 2025 — even after the SEC voted in March 2025 to stop defending its climate-risk disclosure rules, and even with SEC Chairman Paul Atkins emphasizing a narrower, materiality-focused approach to disclosure generally. That regulatory shift might have been expected to reduce the appeal of anti-ESG climate proposals to shareholders; it does not appear to have done so. Support for these proposals has instead declined slightly, from under 3% in 2024 and 2025 to under 1.7% in 2026.

As with DEI, the framing has shifted toward financial-value language: several proposals now ask companies to assess sustainability or emissions targets using NPV, expected-value, or ROI calculations, including litigation and reputational risk, while at least three proposals asked for a quantified look at the costs and benefits of plastics-packaging policy. The underlying argument is consistent — that these commitments should be justified in shareholder-value terms rather than treated as inherently worthwhile.

Technology and immigration

Two smaller but growing categories reflect broader public debate this year: technology and immigration.

Within technology, AI-related concerns dominate anti-ESG proposals in both 2025 and 2026. A 2025 proposal asking companies to report on the risk of unethical or improper data use in developing and deploying AI drew around 10% support at several companies; a similar 2026 proposal drew comparable support at one company, while a related 2024 version reached roughly 35% — evidence that AI governance continues to draw real shareholder interest even within an otherwise low-support category. New this season: one company received a proposal about its use of software to identify child sexual abuse material, and another received a proposal asking for a report on managing the risk of its products being used to distribute deepfake content, including child exploitation material. Only the deepfake-related proposal reached a vote, drawing about 8% support.

Immigration-related proposals appeared on both sides of the ESG ledger. One pro-ESG proposal tied to immigration policy was excluded by the company but still went to a vote regardless, and did not secure majority support. On the anti-ESG side, a proposal raising concerns about reliance on the H-1B visa program received only 0.23% support. Given continued political attention to immigration policy, more proposals on this theme are plausible in 2027.

4. A Small Number of Proponents Drive Most Activity

Despite the attention anti-ESG proposals attract, they originate from a narrow group of filers. Three activist shareholders account for more than 60% of anti-ESG proposals submitted in 2026, out of roughly 15 activist shareholders submitting anti-ESG proposals in total. The same three proponents were behind about half of 2025's anti-ESG proposals, pointing to a persistent pattern rather than a one-off.

Individual proponents also tend to specialize by topic and spread their proposals across many companies: one proponent filed climate-risk proposals at 12 companies this season, and another filed a charitable-giving risk proposal at seven companies.

Roughly 15 activist shareholders are responsible for the entire population of anti-ESG proposals filed in 2026, and just three of them account for more than 60% of that total — a useful reminder that proposal volume reflects a small set of highly active filers rather than broad shareholder demand.

5. Key Takeaways

The 2026 proxy season extends a trend visible for several years running: anti-ESG proposals are prevalent, and public debate over ESG-related corporate policy remains loud, but shareholder support for anti-ESG measures stays consistently low — averaging under 2% in 2026. That gap between visibility and vote support has not shrunk the volume of anti-ESG filings; if anything, the shift toward financial-value framing (NPV, ROI, litigation-risk language) suggests proponents are adapting their pitch rather than stepping back. Whether that reflects a genuine attempt to build shareholder support, an effort to align with the SEC's current shareholder-value messaging, or a strategy focused on visibility rather than passage, the vote data through the midpoint of 2026 does not show anti-ESG proposals succeeding — but it does show them continuing.

Frequently Asked Questions

Starting in November 2025, the SEC Staff stopped providing substantive views on most grounds for excluding shareholder proposals under Rule 14a-8. Companies still must notify the SEC and proponents of an intended exclusion, but without the Staff's customary guidance on whether that exclusion is legally sound.

No. As in 2024 and 2025, no ESG-related shareholder proposal — anti-ESG or pro-ESG — has passed in 2026. Anti-ESG proposals averaged about 1.7% shareholder support through May 31, 2026.

Climate-related risk opposition (30% of anti-ESG proposals) and proposals tied to corporate views, charitable giving, and customer/employee alignment (25%) are the largest categories, followed by anti-DEI proposals (14%) and healthcare/reproductive-rights proposals (13%).

A small group. Roughly 15 activist shareholders filed anti-ESG proposals in 2026, and just three of them accounted for more than 60% of the total — consistent with a similar concentration in 2025.

Yes. Compared with more strongly worded 2025 proposals that sometimes called for abolishing DEI programs outright, 2026 proposals more often frame requests around net-present-value, ROI, or litigation-risk analysis of DEI and climate commitments — tying the ask to shareholder-value language rather than opposing the policies outright.